This is a follow-up post to Handleman (HDL), A Turnaround Candidate. With the release of Handleman’s latest quarterly report and conference call, I will give you an update on this company to see if it remains a legitimate undervalued turnaround stock.

Stock Category: Turnaround

Ticker: HDL

Share Price: $6.95 (Mar. 9, 2007)

Intrinsic Value: $14.76

Suggested Buy Range (66% of IV): Below $9.74

Market Cap: $141 million

Suspending Dividends to Pay Off Debt

For the quarterly period ended January 31, 2007 Handleman reported in its 10Q filing:

Handleman announced that it has suspended its quarterly cash dividends of $.08 per share on common stock in connection with amending its credit agreement. The Company will redirect its cash flow to reduce outstanding debt, which increased as a result of several investments to diversify the Company’s products and customer base.

Short-term debt increased from $4 million to $88.9 million. The debt is incurred from the acquisition of Crave, distributor of video games.

Shareholders should not be discouraged by the dividend suspension. With Handleman’s current ratio at 1.37, this is a wise decision made by management to pay off debt in order to avoid running into liquidity problems later on. This is the correct way use the company’s free cash flow.

Expanding Customer Base

In the annual report for the fiscal year ended Apr. 29, 2006, Handleman reported:

During the fourth quarter of fiscal 2006, the Company announced that it will provide distribution, in-store merchandising and category management support for music, video and video games to Tesco PLC beginning in April 2007. Tesco, the largest supermarket and general merchandise retailer in the

Tesco will become Handleman’s 3rd largest customer, behind Wal-Mart and Kmart. Tesco is expected to make up about 4% of Handleman’s total revenue. I see this move as a step in the right direction as diversifying and expanding Handleman’s customer base acts to reduce business risks in a deteriorating business environment.

On an unrelated note, Warren Buffett has been accumulating shares in Tesco.

Company’s View on the Music Industry

A decline of revenues from music sales is currently around 9%. Stephen Strome, CEO, described the music industry as currently in a “long-tail”, when asked by a caller to express his view of the music industry at the conference call. Strome went on to say that the sharpest music sales decline is likely to happen in 2007 and reach a plateau before a slower and steadier long term decline. Strome also expressed that the greatest impact on traditional CD music sales is not due to the downloading of music; he believes that the ease of pirating and sharing songs with friends remains the primary cause of declining CD sales. Lastly, Strome said that in addition to unit declines there are also the effects of dollar declines – many albums are being priced at $9.99 or $11.99 nowadays.

Interestingly, large merchants such as Wal-Mart and Tesco (Handleman’s two biggest customers in North America and the

Although technology is changing fast, I maintain that the physical sales of music will be around and this demand should keep category managers such as Handleman in business for a long time to come. This is because the sound quality of downloaded music today is inferior to physically purchased music. Audiophiles have long criticized lossy compression formats such as MP3 and WMA for their poor sound quality. Only until the summer of 2006 have there been talks of Apple selling high-quality music at the iTunes Music Store (iTMS). For this purpose, Apple is planning to use its own Apple Lossless Encoder (ALE), which as its name suggests, compresses music with no loss in quality.

As you can imagine, music compressed with the new Apple Lossless Encoder takes up considerably more space than its MP3 counterpart -- typically 10 times or more. So that means a 40GB iPod is essentially reduced down to a 4GB given that you store every song in ALE format. Furthermore, Apple will be pricing ALE formatted music at a premium to MP3’s. Lastly, the ALE has neither received FairPlay nor DRM support yet. I see Audiophiles continue buying CD’s for the foreseeable future.

In a few years, CD’s and DVD’s will start to be phased out by new mediums such as NAND flash drives. The bottom line is that there will always be demand for high-quality, uncompressed music in the physical form, whether that is in a CD, DVD, or flash drive medium is irrelevant and Handleman will remain a key player in the music distribution business for many years to come.

Valuations & Other Metrics

Price/Book: 0.51

Price/NCAV: 1.30

Price/Cash flow: 1.34

ROA: -3.5%

ROE: -7.8%

Handleman’s valuation stays attractive. Asset-wise, it is trading at half of book value, and is only selling at 1.3 times its net current asset value. The stock is even cheaper when measured in terms of cash flow, trading at a price per cash flow of 1.34 (bargain basement level). To put it into context, companies that trade below a price per cash flow of 10 often are bought out or go private, richly rewarding shareholders when such events take place. There is very little downside to Handleman’s stock price based on current valuations. However, in the case that the annual cash flow suddenly becomes negative and triggers another sell-off, the stock’s net current asset value of $5.47/share will act as a floor for the stock.

Management

Success in corporate turnarounds largely depends on the company’s management. Having a motivated management will tie together all of the other important factors in turning around a business such as having a viable core business, healthy balance sheet, transparent and clean accounting, as well as a strong free cash flow. I have learned much about turnaround situations from Robert Olstein, who has managed the Olstein All Cap Value Fund since 1995 with an annualized return of 15.4%.

To determine management’s quality, I look for three things:

- Executive’s compensation

- Recognition of problems

- Actions

I learned the first tip from Warren Buffett and the second and third from Robert Olstein.

As I discussed in this post as well as the first Handleman post, I believe management fully recognizes the problems that the company is facing and has taken the corrective actions to help solve those issues.

As for executive’s compensation, I will firstly point you to the company’s Corporate Governance Quotient (CGQ) and then show you the executives’ stock options compensations.

The CGQ is an excellent way to quickly see a company’s overall quality in terms of its corporate structure and quality of management. The following categories are used by CGQ to evaluate companies:

- Board of directors

- Audit

- Charter and bylaw provisions

- Anti-takeover provisions

- Executive and director compensation

- Progressive practices

- Ownership

- Director education

As you can see, part of the CGQ rating is derived from the company’s executive and director compensation.

According to Yahoo! Finance, as of Mar. 1, 2007 Handleman’s CGQ is better than 97.5% of Russell 3000 companies and 94.6% of Retailing companies. This is a very high rating for Handleman. My typical criteria are for companies to score in the top quartile or at least 75% above its peers.

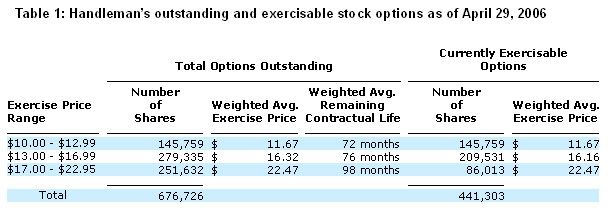

Lastly, let’s take a look at Handleman’s exercisable stock options for its employees.

Table 1 shows the company’s outstanding and exercisable stock options as of April 29, 2006.

What we see here is that the majority of the options granted in the previous years have been at prices significantly above the current market price. Exercise price ranges from $10 to $22.95. Given Handleman’s recent share price in the single-digits, management’s options are worth a lot less if they decide to exercise it today. And indeed, during the fiscal year ended Dec. 31, 2006, with the exception of Sr. VP of HR & Organizational Development who has exercised $11,000 worth of options, all of the other five executives, including the CEO and CFO have exercised no stock options.

By hanging onto their stock options, the executives are showing that they still have faith in the company’s business and are waiting for a recovery in the share price.

Going forward, shareholders of Handleman should pay close attention to the amount of stock options being exercised. If executives across the board are exercising their stock options without the company’s share prices improving that would be the first warning signal for shareholders to sell their shares.

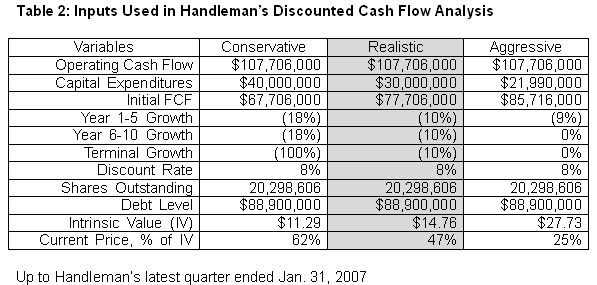

Finding the Intrinsic Value

Table 2 shows the data used to perform a discounted cash flow analysis based on Handleman’s latest reported financial data as of Jan. 31, 2007.

The numbers are based on Handleman’s financial statements, management’s articulation at the conference call, as well as my own estimations. You will immediately notice that the growth rates used in the table are very conservative, even for the aggressive column. Since the future is unpredictable, when performing a long-term analysis such as the discounted cash flow model, conservatism should always be exercised. I am using $14.76 as my sell target until the next quarterly results are released.

Conclusion

Handleman is an understandable business with a wide margin of safety, quality management and rock-bottom valuations. For these reasons it qualifies as a stock pick from The Picky Investor.

----------------------------

Guru disclosure: Franklin Templeton, Third Avenue, Arnold Van Den Berg, Renaissance Technologies own shares in Handleman as of Dec. 31, 2006.

My Disclosure: I, as well as a client, own shares in Handleman (HDL) and Wal-Mart (WMT). I do not own shares in Apple (AAPL) or Tesco PLC (TSCDY).

{kind=link}

{kind=link}

4 comments:

I would watch out with HDL - RIMG has just reveived an $8MM order for CD/DVD replication kiosks in WMT stores. This would cover about 200+ stores and they will be placed in those stores with the most media sales.

My understanding is that the WMT deal is for their photo centers -- to write customer photos to CD-R on demand, and will not be used to burn music CDs (that would involve negotiating new distribution rights agreements with record labels, most likely on a per-click royalty basis -- WMT is better off sticking with the proven HDL distribution model).

Any thoughts on the recent strong declines?

now that the company is trading down around 2.40, do you see it getting a lift anytime soon, or is it on a steady decline for awhile longer?

Post a Comment